What is a Land Contract? A Guide to Land Sale Contracts

Around 36 million Americans have used alternative financing at least once in their lives to borrow money for buying a home. Around 1.4 million of these people have used land contracts to finance their home purchases. Land contracts are also referred to as land installment contracts or contracts for deed.

As a homebuyer, a land contract agreement can seem to be reasonable for you for a number of reasons. These contracts can close more quickly and have lower initial costs than mortgages. This alternative financing option can also be reasonable for you if you cannot qualify for a mortgage. You can also consider a land contract if mortgages are not available for a house or the area you want to live in.

What Is a Land Contract?

So, what is a land contract? How does this alternative financing option work? And what are its pros and cons for real estate buyers and sellers? Find out the answers here.

Land Contract Definition and Key Features

The simplest land contract definition is that it is a written legal contract, referring to a type of financing, used for buying real estate. It is different from mortgages in that it doesn’t involve money-borrowing from a lender or a bank. On the other hand, the buyer will make regular payments to the property owner or seller. Once the purchase price is paid in full, the seller transfers the property’s title to the buyer.

The main features of a land contract arrangement are as follows:

Legal Title: Generally, it is the seller who retains the legal title to the house. The buyer has equitable title and they can possess and utilize the property. The title is transferred to the buyer at the fulfillment of the contract.

Payments: As a buyer, you will be making monthly or yearly payments to the seller. This includes the principal amount, interest, taxes, and insurance. The payment terms will be negotiated and clearly mentioned in the contract.

Default Terms: If the buyer defaults on their payments and the contract is no more than 5 years old or no more than 20% of the payment is made, the seller has the right to terminate it and gain possession. If the contract has exceeded either one of these limits, the seller can only foreclose to receive payments from the proceeds of the sale.

Installment Land Contracts: What You Need to Know

Imagine being able to own a property on simpler terms by making just monthly payments to the seller. That is exactly what installment land contracts suggest. In such arrangements, the seller finances their property to the buyer. An installment land contract can be beneficial in the following situations:

When a homebuyer doesn’t have a good credit score and cannot qualify for conventional financing

When a seller wants to sell their property fast or cannot find lenders to finance it. Common situations include undesirable or undeveloped land.

When both buyer and seller want to keep the closing costs low by avoiding land surveys, title reviews, and attorney fees.

When the market conditions are poor or there is a low money supply.

How Does a Land Contract Work in Real Estate?

While the concept of land sale contract may seem lucrative, it is important to know how does land contract work before taking the leap.

The Process of Buying a Home with a Land Contract

The main steps involved in buying a house on a land contract are as follows:

Find a Land Contract Listing: Finding a land contract house can take time but there are dedicated platforms that share these specialized listings.

Negotiate the Agreement Terms: Once you have identified a property, get the help of an attorney or real estate agent to negotiate the terms of the purchase agreement. The installment land contract must include all the details such as full address, buying price, monthly payments, down payment, payment duration, balloon payments, and default terms.

Conduct Your Research: It is recommended to do your research to avoid any surprises. This includes:

Reading the entire contract & disclosures

Conducting a title search

Utilizing an escrow company

Getting a home inspection

Getting an appraisal

Signing & Moving In: Once find the perfect deal, sign the contract that will give you equitable title. You can occupy and take possession.

Start Making Your Payments: You can make your monthly installment payments directly to the seller or through a service company.

Once you have paid off the land sales contract, the seller will transfer the title deed to you and you will become the owner.

The Role of Buyer and Seller in a Land Contract

When you are considering land contract homes, it is important to understand the role of the buyer and seller.

Since there is no traditional lender involved, it is the seller who sets the requirements for checking the buyer’s credit. Sellers usually offer favorable terms to sell their property faster.

Both the buyer and seller should sign a sales agreement that clearly specifies the terms of the contract.

Every land sale contract is unique so it is important to use custom forms and not standardized forms.

Both buyers and sellers should negotiate the contract, ensuring that the terms do not put them at any disadvantage.

Land contract homes usually offer fewer protections to buyers as compared to mortgages.

Payment Terms and Interest on a Land Contract

It is important to know about the general terms related to payments and interests related to land contract homes before signing the agreement.

Down Payment Amount: The down payment is due at the closing of the term. It can be a fixed amount or a percentage.

Monthly Payments: The contract should clearly mention the amount of installment payments and their periodicity. There should be information on due dates, late fees, and the details of any balloon payment to be paid at the end of the term. There should also be a mention of any penalty if the loan is paid off early.

Interest Rate: The land contract should mention the interest rate. It should also state whether the rate can change or not. If it can, then the time and conditions should be well-defined.

Who Pays Property Taxes on a Land Contract?

Another important question that needs to be addressed when considering this option is who pays property taxes on a land contract.

Property Taxes and the Buyer’s Responsibility

It is the buyer who is usually responsible for paying the property taxes for land contract real estate sales. Eventually, this will depend on the terms of the agreement. In certain situations, it is the seller that pays this tax until the buyer has made the final payment.

Generally, it is the buyer who will be taking care of the property taxes and handling all the maintenance and repairs. The buyer is also typically required to get homeowners insurance.

How Property Taxes Are Handled in a Land Contract Agreement?

As mentioned above, a land contract agreement usually requires the buyer to bear the property taxes. It is important to keep the following points in mind in this regard:

While the buyer doesn’t hold the legal title, they are required to pay the property taxes because they will become the homeowner.

As a buyer, you can take possession and live on the property and use its facilities.

You are required to pay the taxes because you will take over the home ownership.

You will also be responsible for paying the maintenance costs and home insurance premiums.

Pros and Cons of Buying a Home with a Land Contract

Now that you know how does a land contract work, it is important to know that these agreements are not meant for everyone and every situation. An insight into the pros and cons of these contracts can help you determine whether it is right for you or not.

Pros:

Easier to Qualify: These contracts generally have flexible requirements compared to traditional mortgages.

Faster Closing: Closing on land contract homes is usually faster than it is for normal mortgage loans because there is no underwriting process.

Selling Faster: With installment land contract, the seller can sell their property faster. Besides, they can generate a periodic income from the agreement.

Lower Closing Costs: The closing costs are typically lower compared to those involved with standard mortgages. For example, there are no loan origination charges involved.

Cons:

Higher Buying Price: Land contract properties often come with a higher price. They can also have higher interest rates to cover the higher level of risk.

Seller Has Greater Advantage: When you enter a land sale contract as a buyer, you are placing a lot of trust in the seller.

Lesser Protection: These real estate contracts are not as regulated as those financed by traditional mortgages. This means there is less protection in case of foreclosure.

In this arrangement, the legal title is held by the seller until the full payment is paid off. Besides, if you default on the payments, you forfeit your rights to the property.

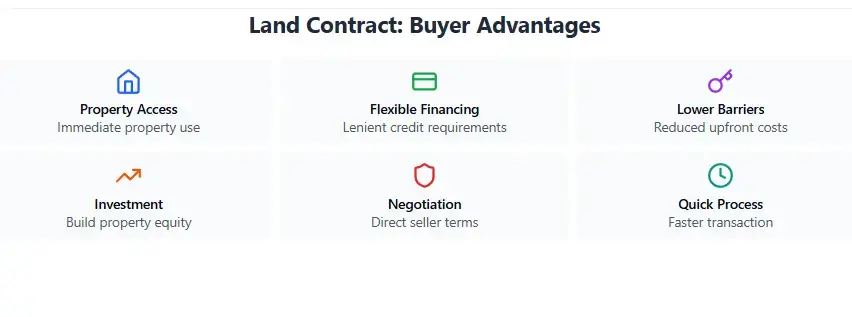

Benefits of Land Contracts for Buyers

There are many reasons why a land contract real estate transaction makes lots of sense for many buyers. Some of its features that can work in your favor as a buyer are as follows:

No Need for Credit Qualification: This is one of the biggest reasons many buyers are attracted to a land contract agreement. You are well-positioned to purchase a house even if you have a low credit score.

Flexible Terms: You are also better positioned to negotiate the terms with the seller. This includes creating a payment schedule that works for you as well as the seller. Even when interest rates can be higher, you can negotiate and lower them as well.

Faster Closing: If you are in a situation where there is a need to move quickly on a property, a contract for deed can be perfect. Since there is no need for bank approval, these contracts have faster closing processes.

Risks for Buyers and Sellers in Land Contract Agreements

Before you sign a land sale contract, it is important that you are clear about the risks involved. Since this approach to buying a property offers flexibility by eliminating the requirements of traditional mortgage loans, it compensates for that advantage by adding the following types of risks:

Risks for Buyers

As a buyer who is exploring houses for sale on land contract, you are open to the following risks:

Limited Legal Protection: These contracts are not as regulated as traditional mortgages. If a dispute arises, the seller tends to have greater advantages.

Option for Balloon Payments: Some contracts can have the seller requiring balloon payments. These are large lump-sum payments that need to be paid at the time of the contract’s completion. You should negotiate with the seller for better terms based on whether you can afford it or not.

Risk of Foreclosure: As mentioned above, if you fail to make your regular payments, there is a high risk of foreclosure. Based on the agreement, the seller may have the right to foreclose on the real estate without even following the legal steps involved in a traditional foreclosure.

Risks for Sellers

As a seller in a land contract agreement, you should be aware of the following risks generally involved in such an arrangement:

Limited Legal Protection: As with buyers, there is limited legal protection for sellers in land contracts. If the buyer defaults, you will have to follow the legal pathway to regain your property and this can be a long and costly process.

High Chances of Buyer Default: These contracts generally attract buyers who cannot qualify for traditional mortgages. Many of these buyers can have bad credit or lack of financial stability, which increases the risk of defaults.

Limiting Reselling Power: If you need quick access to cash, you will have limited powers to resell such a property.

Land Contract Examples and Common Scenarios

The following example sheds light on how a land sale contract works:

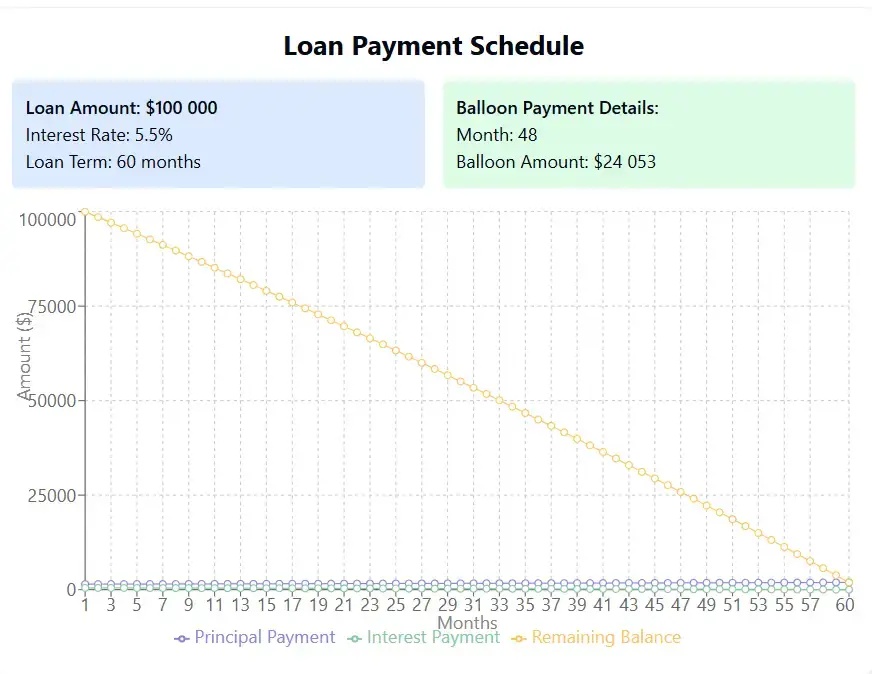

John is a buyer and Williams is a seller. The first scenario has Johan and Williams agreeing to structure the land contract similar to a traditional mortgage where payments are amortized and paid as equated installments over a fixed period of time.

The house is priced at $200,000 by Williams

The terms are 3% interest rate and zero down payment

John will have to pay just over $840 per month for a period of 30 years to close the contract and have the house titled to their name

The second option is to amortize the land contract agreement over a longer duration and have a balloon payment after a certain number of years. This can benefit both the parties. While the buyer can build their credit history and refinance, the seller can get the payments in a much shorter duration.

The balloon payment may be set for a period of 3 years

The buyer pays the same equated monthly installments for 3 years before making a final balloon payment of $187,930

Real-Life Example of a Land Contract in Action

When it comes to exploring examples of land contract homes, Minnesota is a splendid example. Some of the key statistics related to ‘contracts for deed’ transactions between 2005 and 2022 for the state are as follows:

Minnesota is the only state requiring buyers, not sellers, to record their land contract real estate transactions.

These contracts are generally used for buying residential properties.

They are more commonly used for buying low-cost properties.

While 63% of contracts involved individuals, only 18% involved corporate entities.

Minnesota has the fourth-highest number of contracts for deed transactions in the country.

Understanding the Terms of a Land Sale Contract

A land contract can be a good option for you to purchase a property in the following scenarios:

You have completed a thorough title search and found no issues

You need to improve your credit to refinance and purchase the contract later

You cannot qualify for traditional mortgage loans

You have a steady income source or even if it is not regular, you do not have difficulty keeping up with rent in the past

What to Do When a Land Contract is Paid in Full?

When you keep making your regular payments on a land sales contract, you will have equitable title to the property. The seller cannot sell the property to anyone else or subject it to a lien. However, the legal title will stay with the seller. Once the property is paid off in full and all the conditions of the contract are met, the property’s deed needs to be filed with the respective government agency, such as the county register of deeds. The buyer then becomes the property’s owner.

Conclusion

Land contract homes can work as a great alternative for those seeking to buy a property without having to meet the stringent requirements associated with traditional lending. Still, this approach to financing a property comes with its own set of benefits and risks for both the buyer and seller. If you are considering entering into a land contract agreement, it is best to get the help of an experienced real estate attorney or agent.

FAQs:

What is the primary purpose of a land contract?

The main purpose of land contracts is to simplify and speed up the sale/purchase of a property. It can help a buyer to purchase a property when they cannot qualify for a traditional mortgage and a seller sell their property fast.

What are the downsides of a land contract?

There are several downsides to land contracts. They tend to have higher interest rates, fewer regulatory protections, and apparent risks of default by buyers.

Who owns the property in a land contract?

While the buyer has the right to take possession and live in or use the property, the seller continues to own the title in a land contract. The title is transferred to the buyer once the entire contract is paid off.

How is a land contract different from a mortgage?

A land sales contract is different from a mortgage in that it is seller-financed. A bank or a traditional lender is not involved in it. Besides, buyers do not have to go through a bank approval process, thus, speeding up the process for both the buyer and seller.

What happens to a land contract if the owner dies?

In case of the death of the property’s owner, a land contract is still valid and enforceable. You should continue making the payments. When creating a contract, it is recommended to mention that it is binding on the heirs and successors of the parties.