What Is Creative Financing in Real Estate? Types and Examples

What Is Creative Financing in Real Estate?

Whether you are a homebuyer or investor, you have many different financing options to choose from. While the traditional mortgage is the first thought that comes to mind, qualifying for such finance may not be possible for everyone. If you find yourself in such a situation, creative real estate financing may be a good option for you. So, what is creative financing, how does it work, and what are its different types? Find out the answers in this guide.

Creative Financing Real Estate Meaning

It is easy to get around creative financing real estate meaning. It is an alternative or unconventional approach to financing for acquiring a residential or commercial property. This includes a series of different financing methods. Generally, homebuyers and investors utilize these financing options to reduce their financial contributions while securing good interest rates.

Real estate creative financing is focused on benefiting both buyers and sellers, as it bypasses many of the requirements involved in general lending. Some of the key characteristics that make this type of real estate financing special include faster funding, greater flexibility, and higher acceptability for investors who cannot qualify for conventional financing.

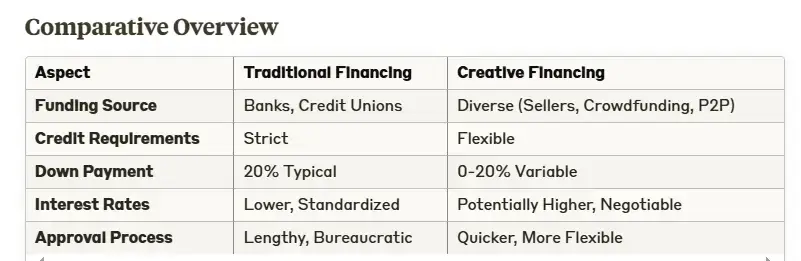

How Creative Financing Differs from Traditional Financing?

Most people understand how traditional financing works. These are loans offered by lenders or banks to finance a part of a property’s purchase price. Such loans are generally secured by the real estate itself and can have adjustable or fixed interest rates.

Creative financing in real estate is different from it. Consider a situation where you want to purchase a house or invest in it but do not qualify for a mortgage due to one or more of the following situations:

You do not have enough capital to make a down payment

Your credit score is low

You cannot afford the high interest rate due to a low credit score

This is where creative real estate financing can assist you in purchasing the property. Usually, there is no conventional bank or lender involved. This type of financing is different from traditional mortgages in that it is not subject to your credit history or even your income. The factors that play a role here include:

Seller’s interest or motivation

The property’s value

Your negotiating skills

The following example should help you better understand it:

You and your partner are looking for buy your first home. While both of you have a stable income, you do not have a credit history or a sizeable down payment saved to meet the requirements of a traditional mortgage. That doesn’t mean that you cannot purchase a house. A creative financing strategy such as ‘seller financing’ can come to your help. All you will have to do is find a seller who is ready to sell their house to you for monthly payments that will be paid directly to them.

The Benefits of Creative Financing for Buyers and Sellers

Real estate creative financing benefits both property buyers and sellers. As a buyer or investor, you can acquire a property with greater ease. It provides a flexible funding option. It allows you to access financing even if you have a low credit score. On the other hand, sellers can benefit from faster property sales. Offering flexible terms to buyers can help sellers reduce the time their property remains on the market.

Types of Creative Financing in Real Estate

Before you consider real estate creative financing to purchase a property, it is important to know about the different options available to you. This includes seller financing, lease options, subject-to financing, wraparound mortgages, hard money loans, and creative financing for commercial real estate transactions.

Seller Financing

Seller financing is a popular creative real estate financing option where the seller acts as the lender. Also known as owner financing or carryback, it is the seller that provides a loan to the buyer to finance their purchase. In this case, you will be making monthly payments to the seller and not a bank. You can consider this option if you cannot qualify for traditional mortgages or seek more favorable terms.

As an investor or buyer who seeks to minimize their financial commitment and benefit from external funding sources, seller financing can be an excellent option. The key features of this arrangement are as follows:

The seller holds the purchase note

You will be making monthly payments to the seller until the purchase note gets fully paid off

Ideally, the seller owns the property outright and is interested in generating long-term passive income

Lease Options or Rent-to-Own Agreements

Lease options or rent-to-own agreements are types of creative financing in real estate that allow you to rent a property while having the option to purchase it at a later date. A part of the monthly rent you pay goes towards building your equity in the property. This equity can be utilized as a down payment when you decide to purchase it.

Some of the key attributes of lease options are as follows:

You can collaborate with a landlord and provide them with the option to purchase their property once the lease agreement concludes

As an investor, you will be building equity through your monthly rent payments

The property owner will be benefitting in the form of regular monthly income

You can have it mentioned in the agreement that a part of your rent payments be credited toward a future down payment

Such an arrangement can also be beneficial for those who want to test a property before committing to make a purchase

It can be challenging to find a landlord who is ready to work on this arrangement. Conditions for such a creative financing real estate agreement arise when the owner is facing difficulty in selling their rental property. It will require some diligent research to find such properties. Besides, you will need professional assistance to initiate discussions once you come across a potential property.

Subject-To Financing

Subject-to financing can also be a valuable option for creative financing for real estate that can work in favor of both parties. Such a situation involves the sale of a property that has an existing mortgage. When a seller sells you a “subject-to” property, you will take over its ownership without assuming responsibility for the debt related to the existing mortgage. It is the original owner who continues to hold responsibility for the mortgage. As the new owner, you can take possession of the property.

This arrangement is beneficial for the original owner in that it can help them make additional mortgage payments while also covering the property’s maintenance costs. By ensuring they are able to continue making their mortgage payments, they can avoid foreclosure. This can further protect their credit score from taking a hit.

Wraparound Mortgages

Imagine a situation where John has a mortgage balance of $80,000 and wants to sell his home for $200,000. His mortgage has a 3% fixed interest rate. John and Mandy (buyer) agree to enter a wraparound mortgage situation where John will finance a loan. They agree to a small down payment of $10,000 and the rest $190,000 is offered as a wraparound mortgage at an interest rate of 5%.

In such a situation, Mandy will make a monthly payment to John who will then use the funds to keep paying his original mortgage. The difference of 2% in interest rates between the two mortgages will act as his profit.

Thus, wraparound mortgages combine an existing mortgage outstanding with an additional loan that the seller offers. In these types of creative financing in real estate, you will be making monthly payments to the seller. The seller will use the payments to make further payments to their lender and keep the remaining funds. A wraparound mortgage can be beneficial for you if you cannot qualify for a new loan or do not want to bear high refinancing costs.

Hard Money Loans

Many people, when they think of creative financing for real estate for investment, think of hard money. It simply means borrowing money from a source that is neither a bank nor any financial institution. Many investors are drawn to this creative financing option because it has simpler qualifying requirements as compared to traditional lending. Such types of loans do not require you to have a minimum credit score.

Creative Financing for Commercial Real Estate

Creative Financing for commercial real estate has gained widespread popularity among business owners.

Imagine a situation where an aspiring entrepreneur wants to open a restaurant but doesn’t have the capital required to purchase a commercial property. The entrepreneur finds the perfect real estate for their planned restaurant. They can negotiate a lease option with its owner where they will rent the space for a fixed period. With creative financing, you can include a clause in your agreement where you have the option to purchase the property at a fixed price when your lease term ends. You can further include a clause that states that a part of your monthly rent will go down toward building equity in the property.

Some of the common creative financing options sought by business buyers include:

Earnout Financing

It is an agreement where the buyer and seller agree on a specific amount to be paid to the latter based on the company's performance after the completion of the transaction. They are typically preferred in case of businesses in the middle of a turnaround situation or based on the potential of a business, not its history of cash flow.

These creative loans are versatile in that they can be structured in different ways. They can depend on various financial factors of the company, including:

Revenue

Net income

Gross profits

Mezzanine Financing

When commercial mergers and acquisitions are involved, companies can consider mezzanine financing as an alternative form of financing. In such creative financing real estate transactions, the lenders are generally high-net-worth individuals who seek a high ROI. Therefore, you can expect these financial arrangements to have high interest rates. One of the reasons for the higher interest rates is the limited requirement for collateral.

Seller Financing

Seller financing is also a common type of creative financing for commercial real estate. More and more business buyers are looking for sellers who are interested in such a financing option. These arrangements typically range in duration from 5 to 10 years.

When it comes to commercial seller financing, balloon payment is sometimes included in the terms to give the buyer time to get the business up and running. This payment is usually required 3 to 5 years after the purchase date.

Creative Financing Real Estate Examples

The following example of seller financing sheds light on how creative financing real estate transactions work:

Consider that you are negotiating a seller financing agreement with a property owner. The terms are a 10% down payment for a prime property in a hot market. You maintained and rented the property and it generates $1,500 every month. On the other hand, the seller finds the deal beneficial for them because they get their monthly payments without having to play the role of a landlord.

Thus, creative financing in real estate investment can benefit both the buyer and seller.

Creative Financing in Real Estate: Pros and Cons

Some of the important pros and cons of creative real estate financing are as follows:

Pros:

Faster Approval: These real estate financing options usually get approved faster than traditional mortgage applications. This makes them excellent options when lucrative real-estate opportunities present themselves for a very short time.

Flexible Terms: This type of financing generally offers flexible terms. It can accommodate buyers and investors with lower credit scores or nonconventional income sources.

Negotiable Terms: As an investor or buyer, you can directly negotiate the terms with the lender. This helps you overcome any of the rigid conditions that come with conventional mortgages.

Cons:

Shorter Payment Terms: Many creative financing real estate situations involve shorter repayment periods.

Higher Interest Rates: These real estate financing options usually have higher interest rates than their traditional counterparts. This means you should be ready to pay more in terms of your periodic payments.

Higher Risks: Firstly, there is lesser regulatory oversight over these financing options. Secondly, there is a high potential for foreclosure if there is a default.

Benefits for Buyers

As a homebuyer, it is important about the most important ways different types of creative financing in real estate can benefit you. This includes:

Easier Property Ownership: Even if you do not have the initial capital required to make a down payment or your credit score is low, creative financing for real estate can make it easy for you to buy a residential or commercial property.

Flexible Financing: Wraparound mortgages and other financing options provide highly flexible terms. These alternatives can make the buying process simpler and less stressful.

Advantages for Sellers

One of the main reasons real estate creative financing is so popular is that it benefits sellers who find themselves in special situations where the traditional loan is not a feasible option. The most important benefits of these funding options for sellers include:

Selling Faster: Subject-to financing, lease options, and other such funding solutions can help you sell your property faster. They can help reduce the amount of time your house stays on the market.

Increased Potential for Profits: Seller financing, equity sharing, and other forms of creative financing for real estate can help owners increase their ROI.

Potential Risks and How to Mitigate Them

As mentioned above, creative financing in real estate comes with certain types and levels of risks. This includes:

Increased Cost: This type of real estate funding is usually more expensive than conventional financing. These higher costs are associated with higher interest rates and additional fees.

Risk of Default: With certain creative finance options, defaulting on payments can sometimes mean losing any initial or additional payments you may have made.

Risk of Damaging Relationships: If the creative funding solution involves lending capital from friends or family, any issues arising during the term of the agreement can affect the relationship.

Complicated Legal Landscape: These financing methods mostly involve complicated legal agreements. This can make them difficult to navigate and thus require professional assistance.

When it comes to mitigating the risks associated with creative financing real estate transactions, it is recommended to follow these tips:

Seek professional assistance from real estate financial advisors or attorneys with previous exposure to creative financing.

Negotiate and clearly outline the terms and duties in the financing or sales agreement.

Conduct due diligence, which includes performing thorough background checks on both the buyer and seller. Buyers must ensure they have the financial ability to meet their obligations as laid down in the agreement.

It is further recommended to consider other alternative options, such as buying outright for cash or exploring conventional financing. Consider the risks, benefits, and long-term impact of both traditional and creative financing in real estate transactions.

Conclusion

Creative financing provides you with the opportunity to explore funding options outside the box. These funding solutions are specifically valuable for those who cannot qualify for traditional mortgages or loans. They provide greater flexibility and quicker access to funding. While addressing the unique borrowing challenges faced by buyers, these financing methods can also be beneficial for sellers. They can help them generate income, sell property faster, and overcome market conditions.

FAQs:

Is creative financing illegal?

No creative financing for real estate is not illegal.

How does creative financing work?

Creative financing is a non-conventional approach to funding a real estate purchase or sale. It involves a buyer or investor purchasing a property without utilizing a traditional mortgage or loan. This type of funding is designed to help both buyers and sellers benefit from more flexible terms when buying or selling real estate.

Is creative financing suitable for first-time buyers?

While creative real estate financing is suited for first-time buyers, it is more important to consider a buyer’s financial situation. As a first-time buyer, you should also take the right steps to assess the value of the property you plan on purchasing.

Can You Use Creative Financing for Commercial Properties?

Yes, creative financing can also be used for acquiring commercial real estate. Earnout financing, mezzanine financing, and seller financing are common options used for financing and acquiring businesses.