How to Buy a Home with No Money Down: Options for Every Buyer

Is It Possible to Buy a Home with No Money Down?

A down payment is an important step in the process of becoming a homeowner. It is a lump sum amount calculated as a percentage of the mortgage on the property. A down payment is traditionally around 20% of the total amount you borrow from a lender or bank. So, if you seek a mortgage of $500,000, you will generally be required to pay a down payment of $100,000 (20%) to purchase the property. However, it is not easy for everyone to afford such amounts as initial payments. This is where the question arises in many homebuyers’ minds, how to buy a home with no money down?

The answer to this question is a ‘yes’. There are a few cases or situations where you may be eligible to purchase a house with no down payment. The common methods include Veterans Affairs (VA) loans and the USDA loans. Besides these government-backed mortgages, you can also benefit from a few creative financing options.

What Does "No Money Down" Mean in Real Estate?

Coming to the question of how to buy a home with no money down, it is important to understand what the term ‘no money down’ means in the real estate world. A home loan with ‘no money down’ means that there is no need to make a down payment at closing. While it may sound appealing to many potential homebuyers, it is something that is hard to get, especially in an economic climate where banks no longer prefer offering them to most customers. However, this does not mean that it is impossible to find no money down home financing options.

Understanding Zero-Down Payment Programs

Whether you are looking for an answer to the question of how to buy a house with no money down first time home buyer or as a second-time home buyer, you should know about the zero-down payment programs. A zero-down mortgage allows potential homebuyers to buy a house without the need to make a down payment. Programs offering such mortgages are generally backed by government agencies, including:

The Department of Veterans Affairs (VA)

The U.S. Department of Agriculture (USDA)

These agencies provide lenders with guarantees to minimize their risks.

Zero-down mortgages help lower the upfront cost, thus making homeownership more easily accessible, especially to first-time home buyers who have limited savings. It is important to know that these loan programs still have eligibility conditions related to:

Your credit score

Income

Debt to income ratio

It is also important to keep in mind that zero-down mortgages come with higher monthly payments and you will usually have to bear higher overall interest costs over the entire lifespan of the loan.

Pros and Cons of Buying a Home with No Money Down

While evaluating the question of how to buy a home with no money down, it is important to weigh its pros and cons before.

Pros:

A zero down payment mortgage allows you to purchase a house without the need to pay a large amount of money from your savings.

You can own a home sooner than you could have if you had to save up for the down payment.

A no down money loan can prove to be a strategic investment. You will gain equity in a property without the need to invest a big amount from your savings.

Cons:

Since you are borrowing more money with zero-down payment, you will be paying more interest compared to making an initial down payment.

There is a good chance you could have afforded a more expensive home if you were able to put money down.

Since you put down less money, you will have less equity in the property.

You can expect additional fees.

How to Buy a Home with No Money Down?

Explore the different ways you can buy a house with no money down.

Government-Backed Loan Programs

Some of the popular government-backed loan programs that can help you purchase a home with no money down or minimal down payment are as follows:

VA Loans

A VA loan is meant for military veterans, active-duty service members, surviving spouses of deceased veterans, and previous or current members of the National Guard or Reserve. The loan is insured by the Department of Veteran Affairs. If you put down less than 5%, your VA funding fee can be significantly low.

You can qualify for a VA loan if you meet the following service requirements:

At least 181 consecutive days of active service during times of peace

At least 90 consecutive days of active service in times of war

Over 6 years of service in the National Guard or Reserve or 90 days or more within the scope of Title 32 orders

You received a discharge through reason of service, such as connected disability

A qualifying spouse of a service member who passed away in the line of duty or from some service-based disability

Besides, different lenders can have different minimum credit score requirements.

USDA Loans

If you want an answer to the question of how to buy a house with no money down first-time home buyer, you can consider the USDA loan program. It is backed by the U.S. Department of Agriculture. If you are eligible, you can get a loan with zero down payment requirements and lower fees.

Some of the main qualifying requirements are as follows:

The house must be in a suburban or rural area

The property cannot be a working farm

It should be a single-family unit

The house should be used as your primary residence

Your combined household gross income should be limited to 115% of the median income in the region

Your debt to income ratio should be 41% or lower

Your home payments, including the monthly payments, taxes, insurance, and homeowners’ association fees, must not be 29% of your income

You will also have to meet the minimum credit score requirements to qualify for a USDA loan.

Federal Housing Administration (FHA) loans are insured by the FHA, a part of the U.S. Department of Housing and Urban Development. If you can make a down payment of 3.5% or more, you may be eligible for this government-backed mortgage program.

First-Time Home Buyer Options

If you are a first-time home buyer, there may be a number of options for you if you are considering how to buy a house with no money down first-time home buyer. This includes government-backed mortgages and creative financing methods.

VA Loan or USDA Loan

One of the simplest ways first-time home buyers can own a house with no money down is by using a government-supported mortgage. If you are a veteran, an active military member, or an eligible spouse of a deceased veteran, you can avail zero-down payment to purchase a house.

USDA loans are perfect for those living in rural or certain suburban areas. This loan program also comes with the benefit of zero down payment.

Down Payment Assistance (DPA) Programs

Many potential homebuyers are unable to make a down payment because they find it difficult to save for it. There are both federal and state level down payment assistance (DPA) programs that can help you if you are one such homebuyer. Key benefits of such programs include low-interest loans and grants to cover closing costs and down payment.

For example, the HomePath Ready Buyer program can provide you with up to 3% of your closing cost.

Besides benefiting from these programs, you can also seek financial help from a family member to put down money for your mortgage. It is recommended to have the donor create a gift letter to be presented to the lender.

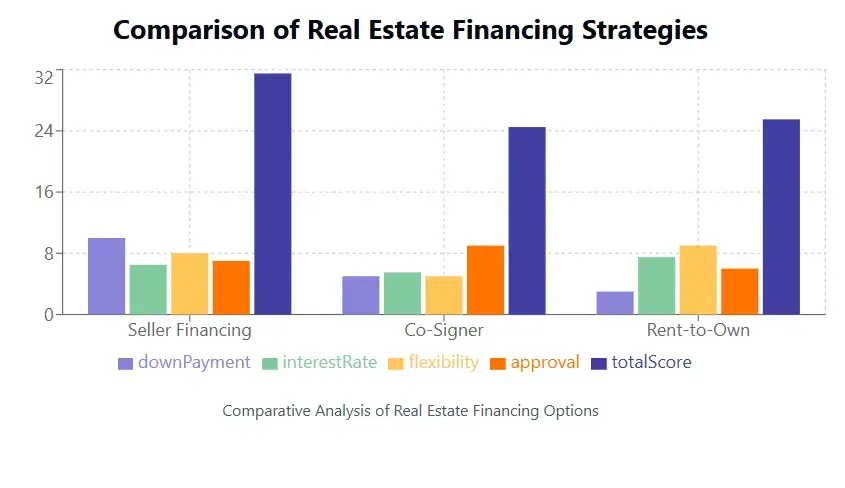

Creative Financing Strategies

If you cannot qualify for a no money down loan using the above-mentioned programs, there are still additional strategies to help you. Creative financing strategies can either help you lower your down payment or work out a zero-down payment arrangement.

Examples of creative financing approaches are as follows:

Seller Financing: This is one of the most common ways to purchase a property with no money down. The seller can finance the purchase price and all you will have to do is make periodic payments to the seller until the house’s price is fully paid off.

Using a Co-Signer: If you have a co-signer with a good credit score, you can qualify for better mortgage terms. In the right conditions, your down payment may get significantly reduced or you may also be able to get a zero down payment offer. Additionally, the interest rates can also be low in such a scenario.

Rent-to-Own Agreement: This is a popular arrangement that can address the question of how to buy a home with no money down and bad credit. A part of your rent is paid in building equity in the property. Once you are ready to purchase the house, the equity you have built over time can be used as your down payment.

How to Buy a Home with No Money Down and Bad Credit?

If you are thinking of how to buy a home with no money down and bad credit, the answer is that you have a few options that can work for you. Certain programs, such as FHA loans can simplify homeownership. Still, a lot will depend on your credit score.

Combining Low Credit Score Solutions with Zero Down Payment

Generally, when someone applies for a home loan, a low credit score usually means a higher down payment. Still, there are certain government-backed programs as well as creative financing options that can help you avail zero or minimal down payment even when you have a low credit score.

Government Programs for Buyers with Bad Credit

There are several government programs that can help homebuyers with bad credit purchase a house. Some of the most commonly used programs include:

FHA Loans: This government-backed mortgage program has some of the lowest credit score requirements. You may be eligible for it even if you have a credit score of 500. If you have a credit score of 580 or higher, you may require just a 3.5% down payment.

USDA Loans: As mentioned above, the USDA loans are targeted at homebuyers in rural and suburban areas. These loans do not require you to make a down payment. Generally, it accepts potential homebuyers with up to 680 credit score.

VA Loans: If you are a veteran, in active service in the military, or you are a spouse of a deceased veteran, you may be eligible for VA loans. There are several programs under this head and you can usually get a loan without a down payment.

Creative Options for Overcoming Credit and Down Payment Hurdles

If you want to explore creative options when thinking of how to buy a home with no money down and bad credit, you can opt for one of these strategies:

Owner Financing: Consider a scenario where you can negotiate the terms with the seller, where the seller acts as the lender. Such an approach, where the owner finances your purchase, does not require you to go through a bank approval process. Many sellers are eager to sell their property quickly and are ready to offer this creative financing solution.

Subject-To Financing: This is another lucrative approach to buying a house without going through the hassles of credit qualification typical to traditional mortgages. Sellers who have overdue mortgages or are facing a threat of foreclosure can be ready to enter into a subject-to financing arrangement. As a buyer, you can pay off their monthly payments while getting a chance to own the property without the standard loan obstacles.

Installment Contract: This is a creative financing agreement where you can take possession of a property while making periodic payments to the owner. It can also have a balloon payment at the conclusion of the term. If you have bad credit, this approach can also help you improve your credit score. At the same time, it doesn’t require you to make a big initial payment.

Seller Carry-Back Financing: Similar to owner financing, this creative financing option also helps you address the question of how to buy a home with no money down and bad credit. The seller extends a part of the buying price as a loan to the buyer and it can benefit both parties by simplifying and speeding up the process.

How to Buy a Foreclosed Home with No Money Down?

When you come across a foreclosed home listing, it means that the lender has repossessed it.

What Are Foreclosed Homes?

A foreclosed house is a property that has been repossessed by the lender after its owner defaults on the mortgage. If you are a potential homebuyer who seeks a good deal on a property, you should consider this option. Often such lenders are ready to sell these properties at favorable terms to recover their losses. This is a good option for you to consider the question of how to buy a foreclosed home with bad credit and no money down.

Financing Options for Foreclosures Without a Down Payment

There are a number of options available to you if you want to finance a foreclosed house without having to make a down payment. This includes:

FHA Loan

You can apply for an FHA loan when buying a foreclosed home. 203(k) loan is a special type of FHA loan offered for high-risk real estate-owned (REO) foreclosed properties. It is important to know about the different fees associated with this loan before applying.

HomePath Program Under Fannie Mae

If you are thinking of how to buy a foreclosed home with no money down, you may want to consider the HomePath program. It will require you to complete an essential online home-buying course. You can then get up to 3% in closing-cost assistance to buy a foreclosed house.

HomeSteps Program Under Freddie Mac

This program involves buying bank loans and pooling them to provide securities to investors. The HomeSteps program markets foreclosed properties owned by Freddie Mac. It is available in the states of Florida, Alabama, North Carolina, South Carolina, Georgia, Kentucky, Illinois, Texas, Tennessee, and Virginia. This loan program does not require you to go through an assessment.

Risks to Consider When Buying Foreclosed Properties

Investing in foreclosed properties may seem like a lucrative opportunity, as lenders are often eager to sell them off at a much lower price than the market value. Still, there are certain risks associated with buying a foreclosed house.

When considering how to buy a foreclosed home with bad credit and no money down, it is important to know about the risks associated with such a property:

Buying Them “As-Is”: Foreclosed properties are sold on an “as-is” basis. You will be responsible for carrying out any pending repairs or maintenance. If there is extensive damage to the property, you will have to foot the bill.

No Inspection: Since there is no opportunity for a pre-inspection, you can never know what condition the property is in or whether the entire roof needs a replacement.

Hidden Liens: If there are pending property taxes, HOA dues, or other liens, you may have to spend a lot after buying the property.

Lack of Knowledge of Actual Value: There is generally a dearth of information about a foreclosed property as compared to other real estate. It may be near-impossible to get its fair market value.

Whether you are considering the question of how to buy a vacation home with no money down or how to buy a 2nd home with no money down, the process of purchasing a foreclosed house is often complicated. For example, some of these properties have redemption rights fixed to them. The previous owner is likely to have the right to reclaim it even after some time of foreclosure.

How to Buy a Home with No Money Down for First-Time Buyers?

If you are exploring your options for how to buy a house with no money down first-time home buyer, the following tips should help you:

Exploring Your Eligibility for First-Time Buyer Programs

To be considered a first-time homebuyer, you should meet the following conditions:

You have not owned a house over the past 3 years

You do not own any investment or second property as a sole or joint owner

You do not own solely own any marital home

Besides the three-year requirement, you may also need to fulfill the following conditions to qualify for many first-time homebuyer programs:

Minimum credit score of 620

A low debt to income ratio

Capable of paying 3.5% in initial payment

Verifiable, regular income with a minimum 2 years of employment history

How FHA Loans Can Help with Low Down Payments?

If you are exploring your options for how to buy a house with no money down first time home buyer, you should consider FHA loans. While they may not offer a true zero down payment option, a down payment of 3.5% on the borrowed money is not too high.

Benefits of Partnering with a Co-Buyer or Co-Signer

As mentioned above, there are certain advantages of including a co-signer or co-buyer in your loan application when buying a house. Such a proposition makes perfect sense in the following scenarios:

Both of you have equal partnership in the house and can benefit from the loan

One of the co-buyers has a lower debt to income ratio

One of the co-signers has a good credit score

Co-signing a mortgage is ideal when both parties will have their name on the property. Besides, both must be in agreement to share the responsibility of paying off the loan. Such an arrangement can not only increase your buying capacity but also help you get a lower interest rate.

Conclusion

Buying a house is a big event in your life. If you have a reliable source of income, even if it is not regular, there are certain loan programs that can help finance a home purchase. There are many programs that can enable first-time buyers, those with bad or no credit, and even those with no down payment money to turn their dream of owning a house into reality. This includes government-backed and creative financing solutions that require minimal or zero down payment based on your situation. When you have the right experts on your side, it can become easier to find answers to the question of how to buy a home with no money down.

FAQs

What credit score is needed to buy a house with no money down?

If you have a credit score of 640 or more, you are well-positioned. You can find many loan programs, both private and government-based, to help you with zero or minimal down payment.

Is it possible to get a home loan without a down payment?

Yes, there are many scenarios where a home loan may be possible without the need to put down an initial payment. Examples of such programs include VA loans, USDA loans, and creative financing.

How much of a down payment do I need for a $300,000 house?

If you have a good credit score and meet all other conditions, you can expect to pay only $9,000 initially. If your credit score is low, you should expect to pay a higher down payment, which can be as high as $60,000.

What is the easiest home loan to get?

Government-backed loans are among the easiest home loans to get. If you do not qualify for any one of these, you should consider creative financing options. These financing solutions have relatively easier qualifying terms but they can have higher interest rates and slightly higher risks.

What type of loan is best for first time buyers?

FHA loans are widely popular with first-time homebuyers. They have low down payment and credit score requirements.

News insight

Feb 26, 2025

Feb 26, 2025How to Find the Fair Market Value of a Home: A Complete Guide

Learn how to find the fair market value of a home. Discover tools, tips, and methods for determining...

Feb 25, 2025

Feb 25, 2025How to Buy a House with Bad Credit: Tips and Strategies

Learn how to buy a house with bad credit. Discover strategies for first-time homebuyers, no money do...