How to Buy a House with Bad Credit: Tips and Strategies

Is It Possible to Buy a House with Bad Credit?

Buying a house is one of the biggest financial and life-changing decisions that most people can make. If you are at that point in your life where you want to move on to the next stage and purchase and live in your own house, you will want to explore the mortgage or loan options available to you. Qualifying for a mortgage will require a credit score evaluation. If you have a credit score of 500 or less, it can be difficult for you to get approved for a loan. Many potential homebuyers find themselves in such a situation and want to know how to buy a house with bad credit.

So, the answer to the question of whether you can buy a house with bad credit is yes. There are some lenders or methods that can facilitate bad credit finance with more flexible qualifying requirements but at higher costs. While you may be eligible for a mortgage with a low credit score, you should be ready to pay a higher interest rate.

What Is Considered Bad Credit for Home Buying?

The minimum credit score required to qualify for a mortgage varies from one lender to another and the type of loan involved. Traditional loans require a score of at least 620. There are government-supported loans that tend to have easier credit score requirements.

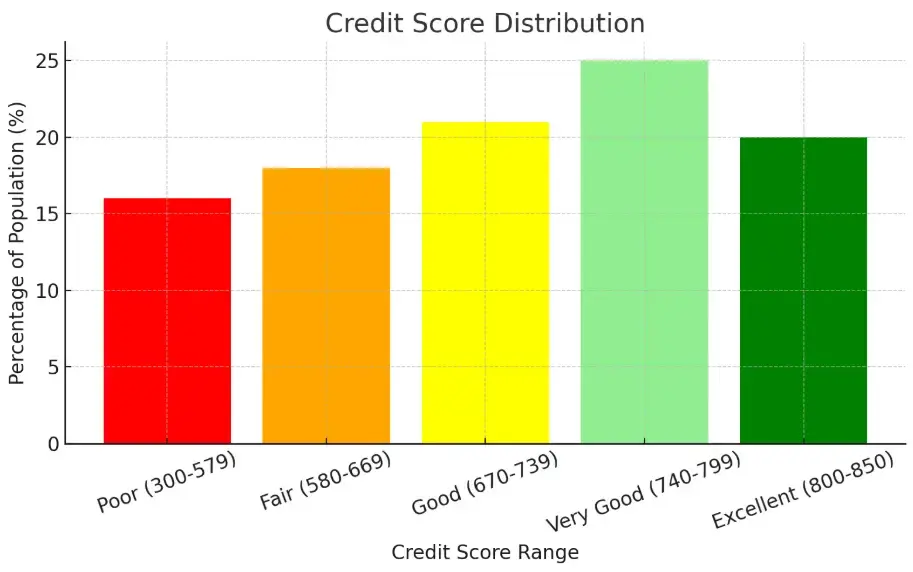

Major credit rating bureaus consider any score less than 670 to be subprime. While a score in the 580-669 range is considered fair in the subprime category, a score of 579 or less is seen as a poor score. If your credit score is less than 500, you can have significant difficulty in getting a mortgage.

How Hard Is It to Buy a House with Bad Credit?

Whether you are considering how to buy a house with bad credit first-time home buyer or with a bad credit history, keep in mind that your score can qualify you only for a specific mortgage loan amount. So, your ability to buy a house generally depends on how much loan you qualify for.

Still, it is important to keep in mind that there are ways to purchase a house by securing a loan even if you have poor credit. If you have enough cash to make a down payment, it can become easier to secure a loan.

Even the choice of the lender affects your ability to get a mortgage. Keep in mind that a bad credit loan typically comes with higher interest rates. So, you should be prepared to pay higher monthly payments.

Can You Buy a House with Bad Credit and No Money Down?

Coming to the question of how to buy a house with no money down and bad credit, the answer is yes. It is possible to purchase a house with bad credit and without making an initial down payment.

Creative financing can be the perfect answer to the question of how to buy a house with bad credit and no money down. There are different types of creative financing solutions. In seller financing, the property owner directly funds the sale for the buyer. Sellers are often motivated for such an arrangement when they are struggling with their mortgage payments or want to get their property quickly off the market.

Such an arrangement can enable you to own a property with minimal or no down payment to begin with. However, the eventual down payment and interest rate are subject to how well you can negotiate the terms with the seller.

Creative Financing Strategies for Buyers with Bad Credit

As mentioned above, creative financing is an excellent option if you want to buy a property with minimal or zero down payment. Here are different creative financing strategies that sellers and buyers generally use in the real estate market:

Seller Financing

This strategy involves the seller financing their house’s sale. The agreement is between the seller and buyer and there is no bank or traditional lender involved. If you are looking for a way how to buy a house with no money and bad credit, this can be the perfect solution. You will not have to make a 20% down payment, as you can negotiate it with the seller.

Lease Option

In a ‘lease option’ arrangement, you will be renting out a house with the option to buy it later. You can opt to build equity in the property using a portion of your rent. This equity can then be used as a down payment in the future when you decide to purchase it.

The following example explains how this creative financing strategy works and addresses the question of how to buy a house with no down payment and bad credit:

A landlord wants to sell their property, valued at $200,000

You can negotiate a leasing option with the landlord

You agree to pay an extra 3% ($6,000) annually as an option fee and a small premium on the monthly rent

These extra payments provide you with the option to purchase the house after a fixed term at the current price

The small monthly premium you pay will accumulate and can work as your down payment at the end of the term

Thus, you will be able to purchase the house at the end of the term without having to pay an actual lumpsum amount as a down payment.

Cash-Out Refinance

If you already own a property, you can consider the option of cash-out refinance on it. This involves borrowing against the equity you hold in the property. This will replace your existing mortgage. This can be a good option since it doesn’t require a significant down payment and comes with a low interest rate. It is also easier to qualify for compared to conventional loans.

Tips for Buying a House with Bad Credit

Besides exploring all the different financing options when finding the answer to the question of how to buy a house with bad credit, it is recommended to follow these tips to improve your chances of qualifying for a loan:

Improve Your Credit Score Before Buying

It is recommended to follow these tips to improve your credit score:

Make sure to keep making on-time payments on your existing loan and credit card payments.

Pay down your revolving debt to build your credit utilization rate. It is best to keep your credit cards open, instead of closing them.

Avoid any new credit applications because they involve hard inquiries and affect your credit score.

Save for a Larger Down Payment

If you can wait before buying a house, it is recommended to use the time to save money to build enough capital for a larger down payment. A larger down payment can increase the chances of mortgage approval even with a low credit score. Generally, lenders approve a loan-to-value ratio (LTV) of 80%, but poor credit can mean a larger down payment is required to cover a greater risk. Additionally, a larger down payment also translates into lower interest rates.

Explore Down Payment Assistance Programs

If you want to buy a house with bad credit and no money down, you can consider down payment assistance (DPA) programs. These programs provide you with money that can be used to cover some of the costs associated with your home-buying experience. Based on the program, you can receive a no-interest loan or non-repayable grant that can be used to pay a part of or all of the down payment and other costs. DPA programs are generally offered by county or city governments or state housing finance agencies.

Some of the common down payment assistance programs that can help you can include:

Grants: As the name suggests, you don’t have to repay this assistance. The amounts received can range from $2,000 to $39,000.

Forgivable Loans: This is generally a second mortgage that doesn’t need to be repaid if you meet its requirements. For example, if you live in the purchased house for a fixed number of years then the lender can forgive the debt. If you refinance the mortgage, sell the house, or move before the period ends, the loan will have to be repaid.

Deferred Payment Loans: These DPA programs offer you a loan that is big enough to cover a down payment. However, it is something that will need to be repaid.

Get Pre-Approved for a Loan Despite Bad Credit

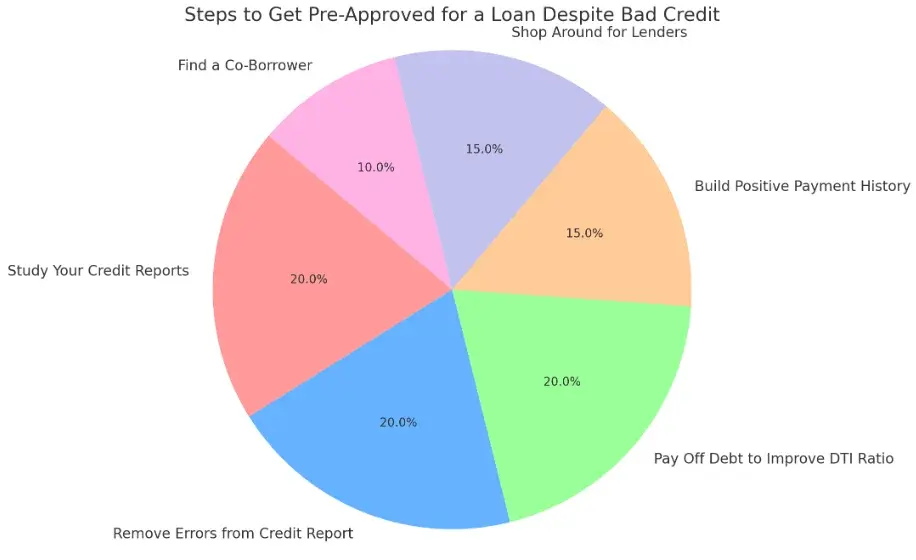

You can take a number of steps to get approved for a loan even if you have a bad credit score. These include:

Study Your Credit Reports: Sometimes your credit reports may have multiple inaccurate entries on them. You can request a free copy of your credit reports from the credit bureaus and review them for any errors.

Remove Errors from Your Credit Report: Once you spot any incorrect entries on your credit report, you can raise a dispute with the bureau to have them removed. Sometimes, collections sent to collections continue to stay on the report even after being paid off. Having them removed can help you improve your credit score.

Pay Off Your Debt to Improve Your DTI Ratio: Lenders also consider borrowers’ debt to income (DTI) ratio. By paying off your debt you can improve this ratio and increase your chances of getting pre-approved.

Besides these steps, it is recommended to build a positive track record of ensuring timely payments, shopping around for the right lenders, and finding a co-borrower to improve your chances of getting pre-approved with a poor credit score.

How to Buy a House with Bad Credit and No Money Down?

Whether you are looking for an answer to the question of how to buy a house with low income and bad credit or how to buy a house with bad credit but good income, there are several effective ways to help you. Some of the simpler options with decent success rates include the following:

VA Loans for Veterans with Bad Credit

If you are a veteran, active-duty service member, or some other kind of military-based borrower, you can apply for a VA loan with the Department of Veterans Affairs. These loans do not require any down payment. Some of the key features of these loans are as follows:

There is no minimum credit score, still, it is preferable to have at least a 580 score

Even if you have a lower credit score, you can expect to get a favorable interest rate

There is a one-time funding fee, which can be included in the closing costs

Regardless of your credit history, VA loans can be the perfect option for you to finance a house if you meet the basic requirements.

USDA Loans for Rural Homebuyers

These loans also perfectly address the question of how to buy a house with no money and bad credit. If you are a homebuyer located in a qualifying rural area, you can avail this type of loan without the need for a down payment. Some key features include:

It is recommended to have a credit score of at least 640 to qualify

Your household income should be limited to 115% of your area’s median income (AMI)

The property must be in a classified rural area

You will be required to pay a 1% initial guarantee fee and a much lesser annual fee

USDA loans are backed by the U.S. Department of Agriculture.

FHA Loans for Buyers with Bad Credit

If you have 500 or higher credit score, FHA loans can help you buy a house with bad credit. This is another government-backed loan and is supported by the Federal Housing Administration and you will need a 10% down payment. If your score is 580 or higher, all you will need is a down payment of 3.5%.

Bad credit score attracts higher interest rates yet the increases in FHA loan rates are much lower compared to those for traditional loans. You will, however, have to cover the upfront and annual mortgage insurance premiums.

Conventional Loans for Buyers with Bad Credit

When it comes to the question of conventional loans on how to buy a house in Texas with bad credit, the simple answer is that you should have a minimum credit score of 620 to qualify. The key is to find the right lender who is ready to assist you.

Some lenders are ready to work with the buyer for a rapid re-score. This may require you to pay off existing debts such as credit card outstanding. The lender can then provide proof of your reduced balance to the credit bureaus. Your credit score will be updated within a few days, helping raise it.

When it comes to the question of how to buy a house with bad credit first-time home buyer, a lender can use unconventional ways to learn about your creditworthiness. They can review your:

Rent payment history

Utility payment history

Phone bill payment records

If you have a proven track record of ensuring on-time payments, your loan may get approved.

Otherwise, the requirements for a traditional loan can make it quite difficult for you to buy house with bad credit. In addition to the down payment requirements, you will have to accept a much higher interest rate. This will affect your monthly payments as well as the overall cost you will be paying for the loan.

For example, if you get a $100,000 mortgage for 30 years at an interest of 3%, you will have to pay $422 every month. At the end of the term, you will have paid $151,777.

The same mortgage at 5% interest will have a monthly payment of $537 and an overall amount of $193,256. Thus, an increase of just 2% in the interest rate will increase your overall payment by over 27%.

Conclusion

Whether you are a first-time homebuyer or you have a poor credit score, it can be difficult to secure a mortgage loan. The answer lies in finding all the different financing options that exist out there for such profiles. You can find options if you have low income, good income, or no down payment to put down initially.

Some of the options that can help you include creative financing, VA Loans, USDA Loans, and FHA Loans. You can also take certain steps to improve your credit score and improve your chances of qualifying for traditional loans. Down payment assistance programs can also help you buy a house with bad credit and no money down.

FAQs:

Can you buy a house with a 500 credit score?

Yes, you can purchase a house with a credit score of 500. However, it will be much more difficult to qualify and you should expect to pay a higher interest rate. You may be able to qualify for an FHA loan, as it requires a minimum credit score of 500.

What is the lowest credit score to buy a house?

While 500 is the lowest credit score required, many lenders will need you to have a minimum of 580 for an FHA loan. So, it will eventually depend on the lender.

Is it hard to get approved for a house with bad credit?

If you don’t have a credit score of 620, it can be hard to get approved for a traditional home loan.

How much money do I need to buy a house with bad credit?

The cash needed to buy a house with bad credit depends on credit score, the house’s price, and the type of loan program you qualify for. For example, FHA loans require a 10% down payment for those having credit scores in the range of 500 and 579 and 3.5% for credit scores of 580 and higher.

How can I raise my credit score 100 points in 30 days?

You can make significant improvements to your credit score in 30 days by paying off your credit card debt, disputing any inaccuracies in your credit reports, and ensuring all your bills are paid on time.

News insight

Feb 26, 2025

Feb 26, 2025How to Find the Fair Market Value of a Home: A Complete Guide

Learn how to find the fair market value of a home. Discover tools, tips, and methods for determining...

Feb 26, 2025

Feb 26, 2025How to Buy a Home with No Money Down: Options for Every Buyer

- Learn how to buy a home with no money down, including options for first-time buyers, foreclosures,...